Site pages

Current course

Participants

General

Module 1. Perspective on Soil and Water Conservation

Module 2. Pre-requisites for Soil and Water Conse...

Module 3. Design of Permanent Gully Control Struct...

Module 4. Water Storage Structures

Module 5. Trenching and Diversion Structures

Module 6. Cost Estimation

Lesson 31. Cost Estimation

Estimating and costing of different soil and water conservation structures are important component of any watershed management plan. The estimation includes calculation and computations of quantities of material likely to be consumed for particular work and also expenses likely to incur for execution of the work. The cost estimation has two components namely material coat and labour cost. The cost estimation forms an important basis for project approval and sanction from competent authority. Moreover, it also helps in economical evaluation of the project.

31.1 Type of Estimate

31.1.1 Preliminary Estimate

This type of estimate is based on reconnaissance survey and practical knowledge and past experience of similar works undertaken. This rough estimate helps in deciding the financial involvement and policy for approval in principle by the competent authority. This estimate briefly presents the cost of major components of work and cost of land, if any separately. A brief report explaining the necessity and urgency of work are also accompanied along with the site plan and preliminary estimates.

31.1.2 Detailed Estimate

This estimate is computed from plan and sectional drawing of the proposed work and is accurate. The quantities of each item for each component of work are calculated using the dimensions taken from the drawing/details. The cost involved for this estimate is known as abstract of cost. The rates of different items of work are taken as per schedule of rates (SOR) available with the department. This schedule of rate is based on prevailing market rate of labour and material for finished item. The most labour involved in soil and water conservation structures are dealing with earthwork. The prescribed earthwork volume that can be assigned to a labour are depends upon the soil type and depth. The details are published by the respective government from time to time. The labour wages are incorporated in the detailed estimate in consultation of prevailing wages in vogue. Detailed estimate consists of working out the quantities of different items of work and their cost as explained below:

Cost Index

Cost index is the value (given in percent over and above) that serves as a factor to take into the account inflation from the period when schedule of rates is published. The usual practices followed is to estimate overall cost including inflation involve the following steps.

Detailed estimation based on scheduled of rates is carried out. This value represents the estimated cost for the time and place for which these rates were published.

This estimated cost is further multiplied by the cost index (The cost index may be negative as well) which vary from time to time and place to place as follow

For example, the detailed estimated cost for a drop structures is computed as Rs. 5.0 lacs on the basis of Delhi Schedule of Rates, 2012 (DSR 2012). The cost index for Hyderabad for year 2013 is 9.39. Thus, if the same structure is to be constructed at Hyderabad in the year of 2013, the overall cost estimate would be = 5X1.0939 = 5.47 lacs.

Details of Measurement and Calculation of Quantities

The proposed work is divided into different sub-heads, e.g., earthwork, concrete work, brick work, rubble work etc. Computation is carried out for each work using the methodology described below. It is important to remember that the dimensions of different components are measured from center to center.

Details of Measurement Form

|

Item No. |

Description or particulars of item |

No. |

Length |

Breadth |

Height or Depth(unit) |

Quantity |

|

|

|

|

|

|

|

|

Abstract of Estimated Cost

The cost of each item of work is calculated from the quantities already computed at a workable rate and the total cost is worked out in a prescribed form (Abstract of Estimate Form) as shown below:

|

Item No. |

Description or particulars of work |

Quantity |

Unit |

Rate |

Amount |

|

|

|

|

|

|

|

In the above forms, the description of each item should be such that in can be expressed explicitly in terms of work, material, proportions of mortar etc. A contingency (@ 3-5 %) is added towards unforeseen expenditure, changes in design and rates etc., which may occur during the execution of work. An expenditure towards work-charged establishment (@ 1.5-2%) may also be added, if required. The grand total thus obtained is the estimated cost of the work. The following format may be utilized for preparation of estimated cost of work.

i) Name of work ii) Location of the work iii) Cost estimate

|

SI. |

Description |

Number |

Measurement

|

Unit |

Quantity |

Unit |

Total cost (Rs.) |

||

|

|

|

|

L (unit) |

B (unit) |

W (unit) |

|

|

|

|

Total

Contingencies (%)

Grand Total

Prepared by

Checked by

Approved by

31.1.3 Revised Estimate

This estimate is also a detailed estimate when the original sanctioned estimate is likely to exceed during the execution of work. The revised estimate is then prepared incorporating the component of work/rate which is responsible for the escalation of the cost. This is necessary for obtaining the additional sanction from the authority.

31.1.4 Supplementary Estimate

This is the first detailed estimate of the work in addition to the original one and is prepared when the additional work is required to supplement the original work as a result of further development during the execution of work. The abstract of cost should show the amount of original estimate and the amount to be incurred in supplementary estimate for which sanction is to be required.

Schedule of Rates

Estimation of the financial cost of works undertaken is usually done on the basis of a Schedule of Rates (SOR) prepared by concerned departments of each state government. The SOR breaks up all work done to build any structure into a series of tasks and provides government approved rates for costing of each task. These are called Task Rates. These task rates are for different types of work (buildings, bridges, roads, dams, irrigation canals, lift irrigation, water supply, sanitation and sewerage). The rates include labour rates (based on minimum wages), rates for materials used, rates for transportation of materials, hiring charges of machines and vehicles, royalty payments for "freely available natural resources" and rates for maintenance of structures. The SOR is used both for:

1. Preparing cost estimates for proposed works; and

2. Valuation of work already done

To use the SOR, the proposed work is needed to break up into a detailed list of all the tasks involved in it. For instance, to construct earthen contour bunds, the work can be break up into its various component tasks, as given below:

1. Excavation of earth

2. Construction of contour bunds with excavated material and

3. Providing stone exits, this in turn involves,

collection of stones (including transportation where stones are not locally available); and

Construction of exits with stones at appropriate places.

Similarly, construction of loose boulder checks involves the following tasks:

Site clearance

excavation of foundation

collection of stones (including transportation where stones are not locally available); and

stacking of boulders to form the boulder check

Construction of more complicated structures like core wall type earthen dams involves tasks:

Site clearance

Survey work

Digging cutoff trench;

Puddle-filling of trench;

Construction of core wall;

Raising outer embankment by laying earth, watering and compaction;

Stone pitching/Sodding;

Construction of rock toe and sand filters;

Excavation for exit weir;

Stone pitching of exit weir; and

Transportation of construction materials including water, clay and stone

31.2 Analysis of Rates

The rates for different items of work comprise of following components.

Material cost: The material cost while estimation is taken as the cost of material at the site that includes material cost, transportation and taxes if any.

Cost of labour: The labour requirement for different items depends on the nature of work. Thus wages as per man-hour or man-day required for particular item of work is estimated and then accounted for total cost of labour.

Tools and plants and sundries: A lump sum provisions are made for tools and plants (T&P) and other small items (sundries) such as water charges, which are not possible to be accounted in detailed estimate. Usually, 3-5% of labour and material costs are considered for this account.

Carriage: The carriage charges to transport material to the remote construction site should be added. This cost components is required where the construction site is not connected with the motorable roads etc.

Contractor’s profit: A provision of 10-15% of total cost including material cost, labour cost, T&P may be added to get the rate per unit of item of work. However, in case where the material is supplied departmentally, contractor’s profit is not applicable to the material cost.

Material required for different items of work

Table 31.1 describes the material required for different items of work specific to soil and water conservation structures.

Table 31.1. Material required for different items of works.

|

Sl. No. |

Particulars of items |

In MKS unit |

|

|

for |

quantity |

||

|

1. |

No. of bricks in masonry work |

1 m3 |

500 nos |

|

2 |

Dry mortar for cement concrete |

1 m3 |

1.54 m3 |

|

3 |

Dry mortar for lime concrete |

1 m3 |

0.40 m3 |

|

4 |

Dry mortar for brick masonry |

1 m3 |

0.3 m3 |

|

5 |

Dry mortar for coursed rubble stone masonry |

1 m3 |

0.4 m3 |

|

6 |

Dry mortar for random rubble stone masonry |

1 m3 |

0.4 m3 |

|

7 |

Stone for rubble masonry |

1 m3 |

1.25 m3 |

|

8 |

Brick for brick ballast |

1 m3 |

370 nos |

|

9 |

Brick ballast for lime concrete |

1 m3 |

1 m3 |

|

10 |

Brick for R.B. lintels |

1 m3 |

450 nos |

|

11 |

Dry mortar for RB works |

1 m3 |

0.45 m3 |

|

12 |

Dry mortar for ashlar stone masonry |

1 m3 |

0.30 m3 |

|

13 |

Brick bats for brick ballast |

1 m3 |

1.10 m3 |

|

14 |

Dry mortar for pointing in brick work |

100m2 |

0.60 m3 |

|

15 |

Dry mortar for C pointing |

100m2 |

0.80 m3 |

|

16 |

Dry mortar for 12 mm thick cement plaster |

100m2 |

1.44 m3 |

|

17 |

Cement for brick flooring |

100m2 |

3.80 bags |

|

18 |

Dry mortar for half brick wall |

100m2 |

3.20 m3 |

|

19 |

Bricks required for 10 cm thick wall |

100m2 |

50 nos |

|

20 |

One bag of cement (50 kg) |

- |

0.035 m3 |

|

21 |

One m3 of cement |

- |

28.8 bags |

(Source: Sharda et al. 2007)

Labour required for different works

Table 31.2 describes the requirement of labour for different items of work.

Table 31.2. Manpower required for different work

|

Sl. No |

Particulars of work |

Quantity of work per day |

Kind of manpower per day |

|

1. |

Earthwork excavation in ordinary soil including disposal upto 30m and lift upto 1.5 m |

3 m3 |

Mazdoor 1 |

|

2 |

Earth filling under floors including consolidation in 15 cm |

6 m3 |

Mazdoor 1, Bhisti |

|

3 |

Earth filling over roofing including ramming |

3 m3 |

Mazdoor 1, mason |

|

4 |

Cement concrete in foundation with brick or stone ballast; lime concrete in foundation |

8 m3 |

Mazdoor 12, mason 1, Bhisti |

|

5 |

Plain cement concrete (1:2:4) |

6 m3 |

Mazdoor 9, mason 1, Bhisti |

|

6 |

RCC 1:2:4 in slabs, beams, lintels and column including bending and binding, reinforcement, centering and shuttering |

4 m3 |

Mazdoor 16, mason 1, Bhisti 2, Blacksmith , carpenter, |

|

7 |

Damp proof course 2.5 cm thick 1:2:4 with 2 coats of bitumen laid hot |

12 m2 |

Mazdoor 2, mason , Bhisti |

|

8 |

I class brick work in cement/lime/mud mortar in super structure |

1.25 m3 |

Mazdoor 2, mason 1, Bhisti |

|

9 |

I class brick work in lime/mud mortar in foundation and plinth |

1.4 m3 |

Mazdoor 2, mason 1, Bhisti |

|

10 |

I class brick work in cement/lime mortar in arches |

0.7 m3 |

Mazdoor 2, mason 1, Bhisti |

|

11 |

Course/random rubble stone masonry in mud/cement/lime mortar in super structure |

1.0 m3 |

Mazdoor, mason 1, Bhisti |

|

12 |

Course/random rubble stone masonry in mud/cement/lime mortar in super structure |

0.7 m3 |

Mazdoor 2, mason 1, Bhisti |

|

13 |

Plastering with any mortar (12 mm thick) |

12 m2 |

Mazdoor 1, mason 1, Bhisti |

|

14 |

Cement pointing or lime pointing |

10 m2 |

Mazdoor 1, mason 1 |

|

15 |

Conglomerate flooring (CC), 4 cm thick cement concrete 1:2:4 over 10 cm thick and cement concrete 1:6:12 over 10 cm thick |

7 m2 |

Mazdoor 2, mason , Bhisti |

|

16 |

Brick flooring 10 cm 1:6:12 CC with sand filling and cement pointed flush |

11 m2 |

Mazdoor 2, mason , Bhisti |

(Source: Sharda et al. 2007)

31.3 Precautions while Using SOR

The strata on which the rate should conform to the classification in SOR

Avoid duplication in the use of rates.

The SOR provides no rates for certain items like placing plastic sheet in an underground dyke or chain link wire in gabion structures. Such items should be costed on the basis of actual market prices.

In all estimates and valuations, the name of the SOR, place and year of publication, item number of the rate used and detailed description of the task should always be mentioned. This ensures cross-checking and transparency.

No extra rates should be applied for providing settlement allowance. The rate given for construction of earthen bunds and dams is inclusive of cost of raising the bund or dam to extra height on account of settlement allowance.

No extra rate is allowed for removing "dead-men" or "tell-tales". While excavating earth, certain portions are left unexcavated as evidence of the situation before work started. For instance, when constructing a dugout pond, the unexcavated portions reveal the lay of the ground before work started and hence the depth to which excavation has been done. Such evidence is necessary for conducting valuation of the structure. After fio e measurements, these portions are removed. The rate for this work includes this cost also and should not be separately charged.

Rates related to lift only apply after crossing the threshold of the initial free lift (usually 1.5 m). Similarly, rates for lead apply after crossing the threshold of the initial free lead (usually 50 m). The quantities of free lift and lead should be deducted from the total lift and lead while applying the rate.

31.4 Estimation of Quantity of Work

For estimating the quantity of work, structures are classified into four groups on the basis of their cross-sectional area and type of material used. Table 31.3 presents classification of various soil conservation structures.

Table 31.3. Classification of various structures for quantity estimation

|

Cross-sectional area |

Type of Material |

|

|

Homogeneous |

Heterogeneous |

|

|

Uniform |

Group I (Contour Trenches & Contour Bunds in One Type of Strata) |

Group II (Contour Trenches & Contour Bunds in Different Types of Strata) |

|

Variable |

Group III (Boulder Check, Gabion Structure, Homogeneous Earthen Dam) |

Group IV (Core wall Type Earthen Dam, Hearting/Casing type Earthen Dam) |

(Source: Dutta, 1966)

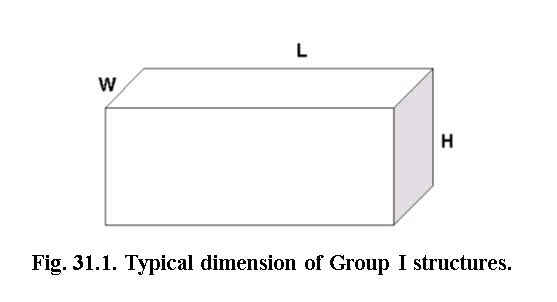

31.4.1 Group I Structures

Fig. 31.1 show dimension of group I structure. When the cross-section is similar throughout the length and material is also same, the quantities can be calculated as:

Volume (V) = Length (L) x Width (W) x Height (or Depth) (H)

V = L x W x H (31.1)

and

Cost of Work (C) = Volume (V) x Unit Rate (R) per volume of work

C =V x R (31.2)

31.4.2 Group II Structures

In these types of structures, the cross-section area is uniform throughout the length of the structure, but material varies. The quantities of various types of materials is calculated separately, as the unit rates for different strata are different. For example, a contour trench with two layers, the upper one and the lower one.

Volume of Upper Layer V1= Length x Width x Depth of Soft Soil Strata

V1= L x W x H1 (31.3)

Volume of Lower Layer V2 = Length x Width x Depth of Hard Soil

V2 = L xW x H2 (31.4)

Total Volume (V) =V1 + V2 (31.5)

Assuming that the rate for digging in soft soil = R1and the rate for digging in hard soil = R2, then the total cost C will be sum of cost of work for upper layer (C1) and cost of work for lower layer (C2)

C = C1 + C2 = V1 x R1 + V2 x R2 (31.6)

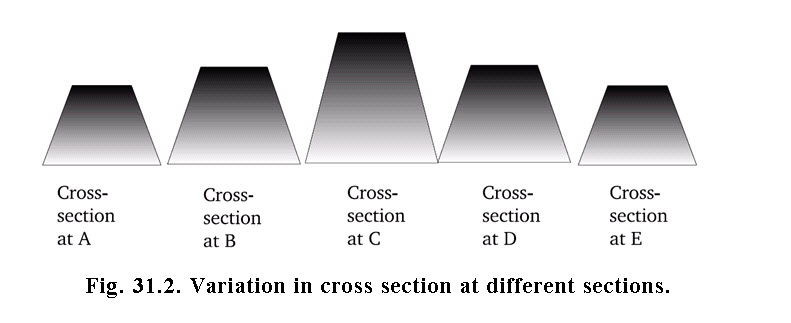

31.4.3 GROUP III Structures

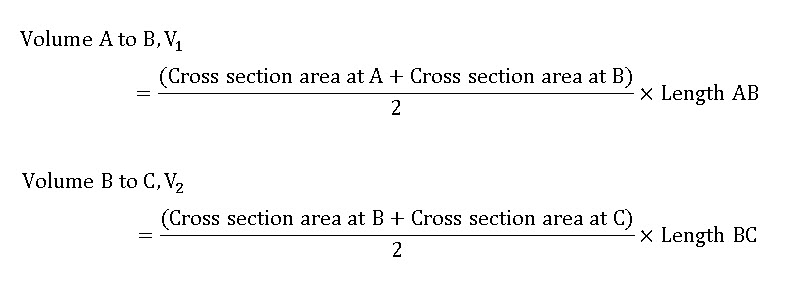

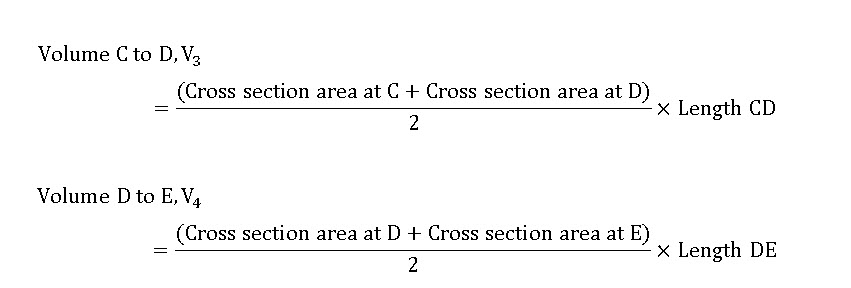

This group of structures has homogeneous construction material but their cross-section area varies across the length of the structure. Here, the structure is divided into several sections and volume of each section is worked out. These volumes are then summed to get the total volume of the structure. The total volume is multiplied by the rate for that particular stratum to derive the total cost. Fig. 31.2 shows a variation in cross-section of the structure at different sections.

Total volume of work = Volume of work of Section A to B

+ Volume of work of Section B to C

+ Volume of work of Section C to D+...

The volume of work of a section is arrived at by averaging the cross section areas of two ends of the section and then multiplying it with the length of that section:

As the material used is the same throughout,

Total Cost of Work = V х R (31.8)

31.4.4 Group IV Structures

In this group, structures have variable cross section area along their length and are also made of heterogeneous construction material. Hence, cost is calculated as:

Calculate cross section area (C1, C2 etc.) for each material (for instance, top soil) at each point;

Calculate average cross section areas of each material;

Multiply this average area with the length between two points to get the volume of the material in that section;

Repeat this for all materials and all sections;

Sum up all volumes of a particular material;

Repeat this for all materials; and

Multiply volume for each material with its unit rate to get the total cost of work.

If the unit-rates for work with different types of material areR1, R2, R3 ..., then:

Total Cost of Work, C = V1 x R1 + V2 x R2 + V3 x R3 + ... etc. (31.9)

Key words: Estimation and costing, schedule of rates, cost index

References

Dutta, B.N. (1966). Estimating and Costing for Civil Engineering, Lucknow.

Khanna, P.N. (1996). Indian Practical Civil Engineers’ Handbook New Delhi: Engineers’ Publishers

Watershed Works Manual, (2007). Ministry of Rural Development, Government of India, pp.226-273.

Mohan, S. C. et al. (2007). Training Manual on Soil Conservation & Watershed Management, pp. 380-393

Sharda, V.N., Juyal, G.P., Prakash Chandra and Joshi, B.P. (2007). Training Manual – Soil Conservation and Watershed Management (Vol II Soil and Water Conservation Engineering). CSWCRTI, 218, Kaulagarh Road, Dehradun.

Suggested Readings

Khanna, P.N. (1996). Indian Practical Civil Engineers’ Handbook New Delhi: Engineers’ Publishers

Watershed Works Manual, (2007). Ministry of Rural Development, Government of India, pp.226-273.

Mohan, S. C. et al. (2007). Training Manual on Soil Conservation & Watershed Management, pp. 380-393

Last modified: Friday, 14 March 2014, 8:39 AM