Site pages

Current course

Participants

General

MODULE 1. Systems concept

MODULE 2. Requirements for linear programming prob...

MODULE 3. Mathematical formulation of Linear progr...

MODULE 5. Simplex method, degeneracy and duality i...

MODULE 6. Artificial Variable techniques- Big M Me...

MODULE 7.

MODULE 8.

MODULE 9. Cost analysis

MODULE 10. Transporatation problems

MODULE 11. Assignment problems

MODULE 12. waiting line problems

MODULE 13. Network Scheduling by PERT / CPM

MODULE 14. Resource Analysis in Network Scheduling

LESSON 2. Systems Concept: Managerial Policy and Decision Making

Managerial policy - functional approach, behavioural approach, decision-making-systems approach - decision-making functions - knowledge and value base, analytical framework for decisions, environment of decisions: certainty and uncertainty - methodology of decisions - complete certainty methods, partial information methods, extreme uncertainty methods.

1. MANAGERIAL POLICY

Modern management techniques have developed from a unique history of practical and theoretical effort. When the machine-powered factory system became well established Frederick Taylor suggested that the scientific method be applied to all management problems. More specifically, he proposed (1) scientific selection and training of workers, (2) definition of each worker's tasks, and (3) cooperation and division of work between labour and management. Taylor's ideas were known as "scientific management systems" and he was known as the "father of scientific management." As corporations grew, a larger financial base was required and stock ownership became more widespread. Owners soon turned to professional managers to run their organizations. Several theories were developed to explain the role of managers; the important approaches to management are discussed below.

1.1. Functional Approach

This widely held approach holds that management has traditionally been charged with the role of planning, organizing, directing, and controlling the activities of an organization. This approach regard management as a universal process which is readily understood in terms of these fundamental functions which must be performed regardless of the type of organization.

1.2. Behavioural Approach

This human relations approach recognizes that managers are people who work through other people to lead the activities of an organization. In viewing the individual as a sociopsychological being, it concentrates upon behavioral and motivational forces and stresses the art of interpersonal relationships. The manager is a leader of individuals or groups and the human element of organization receives paramount attention.

1.3. Decision-Making-Systems Approach

This approach views a manager basically as a decision maker within an operating system. Management is concerned with the methodology and implementation of decisions that facilitate system goals. The decisions may well relate to both functions (such as planning, organizing, directing, and controlling) and to people, for these subgoals and resources both exist within a systems context. Furthermore, scientific methods of modeling and systems analysis can be followed to reach decisions.

Whereas some management theorists would separate the decision-making and systems approaches, we have chosen to emphasize decision making in a systems context because of its theoretical basis and applied usefulness. Other approaches also exist, but we shall not explore them in any depth. For our purposes, then, we shall refer to management as the process of making decisions and taking action relative to functions and behaviour which direct the activities of people in organized systems toward common objectives.

2. DECISION-MAKING FUNCTION

The decision-making-systems approach has particular scientific and analytical suitability, the concept can be selected from other perspectives.

2.1. Knowledge and Value Base

The idea of management as a science is founded upon several observations. First, the "principles and methodology of management" form an organized body of knowledge. Moreover, much of the current decision methodology has advanced to a logically rigorous state. Second, real-world data are available for analysis. The business world is essentially a laboratory to the management scientist. Third, an objective systematic analysis of the data can often be made. This analysis relies largely upon modern mathematical and statistical techniques. Finally, another experimenter (decision maker) could use the same data and arrive at consistent results.

The association of management with the scientific method involves drawing objective conclusions from facts, and facts come from analysis of data. Therefore, the idea of quantification of data is an important element in viewing management as a science. Computers and management information systems are now providing such a data base for decisions. By means of mathematical modeling and simulation, this decision-making process also allows for experimentation and for testing of hypotheses.

Viewing management from the standpoint of a science, one must conclude that the decision-making methodology can be both taught and learned as can other sciences. People need not be "born managers" to do the job. Education, training, and experience can improve managers' abilities to make optimal decisions. They can learn ways of identifying relevant system parameters, collecting data, and analyzing data that will lead to better courses of action. As decision making becomes more scientific, the importance of clearly defined objectives and systematic analysis also becomes more apparent.

If managers were nothing more than mechanistic robots operating in a computerized laboratory, we might uncompromisingly argue for the full-fledged classification of management as a science. But management decisions are not always based upon an "objective systematic analysis of the data. The same humanistic element of concern for others exists in the engineering, medical, and other professions which we commonly associate with the scientific method. Professional decisions are not always value free - the choice of an "appropriate action" often rests, at least partly, upon an individual or an institutionalized value system.

The incorporation of values into business decisions does not necessarily brand the decision process as nonscientific - nor the results as invalid or unpredictable - for several reasons. First, many business decisions can legitimately be based upon facts that do not carry value-laden implications. This is especially true for numerous routine decisions related to micro, or subsystem, operations. An example of this would be the choice an operations manager must make between two similar pieces of capital equipment with differing initial costs and lifetimes. The chances are that this decision can be made in a fairly objective, systematic manner.

Second, existing legal or environmental controls may accurately reflect individual or organizational ethics. For example, production cost auditors may believe that the intent of the tax laws accurately reflects what their firms "should" pay in federal taxes. Thus they neither overlook legitimate cost deductions nor attempt to capitalize on tax "loopholes." In this case, the applicable laws provide a satisfactory guide to action.

Third, values can be made known and accepted as an underlying standard. Many organizations have identified and adhere to sound values (such as codes of ethics) that are applied in a consistent and predictable manner. In this sense, a broadly based value system acts much like an organized body of knowledge and facilitates a scientific approach to decisions.

Of course, many (perhaps most) value-based decisions are complex. Problems arise when "the law" is an inadequate guideline or when values are not commonly or consistently held. Individual decision makers sometimes narrow organizational concerns to their own self-interests. Others have little sense of distributive justice and their allegiance wavers among the conflicting interests of themselves, employees, stockholders, consumers, society, etc. Decision making in such situations cannot be construed as being truly "scientific." Nevertheless there is even hope for eventually moving these situations a little closer towards a scientific basis through proper education and training of the decision makers. As decision makers gain an improved awareness of the value systems of others, the reasons for differences become explored, some differences are resolved, and others perhaps are more willingly accommodated.

Recognizing that despite value differences a scientific framework for business decisions does have wide applicability, we now go on to examine the analytical framework for decisions in greater detail. As we proceed through the steps we shall note the areas where value system differences come into play.

2.2. Analytical Framework for Decisions

An analytical and scientific framework for decisions implies several systematic steps for the decision maker. These steps are summarized as below.

Define the system and its parameters.

Establish the decision criteria (i.e., the goals).

Formulate a relationship (model) between the parameters and the criteria.

Generate alternatives by varying the values of the parameters.

Choose the course of action which most closely satisfies 'he criteria.

The systems approach to defining the problem (step 1) helps to ensure that the final decisions are as nearly optimal as possible. A system defined broadly may include many tangential aspects of a problem, making it extremely difficult to establish the complex relationships among the variables. Similarly, a narrowly defined problem might omit relevant variables. The inclusion or exclusion of variables depends upon the system goals; if variables have a significant effect on the goals, they should be included as parameters of the system.

In some cases, skilled systems analysts can facilitate the solution of problems by providing the operating manager with specific systems design and programming skills. However, the model user must almost inevitably become actively involved in defining the problem and formulating the relationships (that is, model building) if the solution is to be truly a useful user-oriented one. This requires close communication and interchange of information between the systems analyst and the decision maker.

The establishment of decision criteria (step 2) is of paramount importance for they stem directly from objectives which give purpose and direction to work efforts of the organization. For many years, profits served as a convenient and accepted goal for most free enterprise organizations. Perhaps this was because early models of firm behavior were based almost wholly on economic theory. Today, empirical re- search reveals that organizations have sets of goals rather than single goals and that profits are only one of many possible objectives. Studies identified the following eight types of goals set by industries.

Organizational efficiency

High productivity

Profit maximization

Organizational stability

Employee welfare

Organizational growth

Industrial leadership

Social welfare

There is reason to suggest that social welfare goals have gained more importance as environ mental concerns have become more prominent during the past few years. Social pressures are now strongly limiting the exploitation of resources solely for economic gain and instead are focusing upon the greatest good for the most people over the longest period. Nevertheless, for many organizations within our free enterprise society, profits continue to be a key source of motivation, rewards, and investment capital that underlies a good deal of our nation's economic progress.

Numerous ways exist for classifying objectives, such as economic, social, and political, or individual and organizational. The above listed goals have been classified into: (1) general efficiency, which are specific and largely quantifiable criteria and include organizational efficiency, high productivity, and profit maximization; (2) associative status, which sometimes results as a by-product of action toward general efficiency goals and includes organizational growth, industrial leadership and orgnaisational stability; (3) employees welfare; and (4) social welfare classifications. The study referenced found relatively strong correlations between associative goals and personal or organizational characteristics suggesting that differenced in firm behaviour may be more due to associative status goals than to general efficiency goals, and that actual goals of a business may be related more be related more closely to personal characteristics of the managers than to broad characteristics of the business.

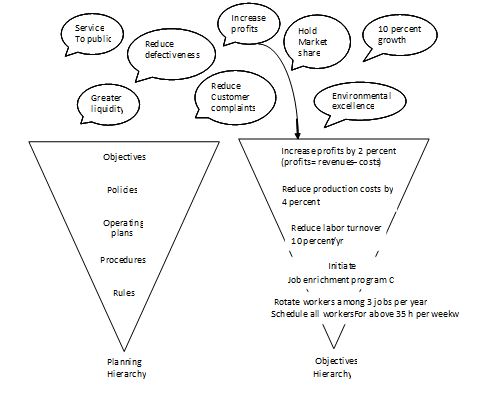

The decision criterion (or set of criteria) flows directly from organizational objectives and should be as specific as possible. A criterion of “maximizing profits” may be adequate as one (economic) organizational goal, but too broad and inadequate for much decision making on an operational goal, but too broad and inadequate for much decision making on an operational level. Fig. 4 depicts the hierarchical structure of goals by comparing it to the familiar upside-down planning pyramid which begins with broad objectives that are ultimately operationalized into specific rules. The figure illustrates the necessity of specific directives such as “Rotate workers among 3 jobs” in order to fulfill broader objectives such as “Increase profits”. Note the subsystem criteria must be consistent with the higher-level goals. If inconsistencies exist in the goal structure, some of the organization’s resources are probably being wasted by the pursuit of contradictory objectives. An example of this would be a power company with vague profit and service objectives. If its marketing group were to promote the distribution of air conditioners while the production capacity was inadequate, neither profit nor service objectives would be achieved. In some cases system criteria, such as “good customer service,” are so difficult to quantify that substitute criteria, such as “number of customer complaints,” must be used. One should clearly recognize and label such measures as indicators or criteria. Otherwise, the substitute criteria may be satisfied, even though the intent of the system criteria is not. For example, a pressured office manager might “reduce the number of customer complaints by 50 percent” by simply adopting a tedious 10-page customer complaint form. Unfortunately, this is not likely to help achieve the organizational objective of better customer service even though the office manager will have satisfied the substitute criteria. Large bureaucracies are often faced with such problems of using substitute criteria because system objectives become institutionalized in terms of formal policies and impersonal regulations. For this reason decision criteria should be reviewed frequently to ensure the surrogate criteria are being used in a manner consistent with total system criteria.

Fig. 4. Decision criteria hierarchy

Source: Monks, J.G. 1977. Operatons Management – Theory and Problems. McGrawhill Book Company, New York.

The formulation of a relationship, or model, for experimentation (step-3) lies at the heart of the scientific decision-making process. Models may be verbal, pictorial, schematic decision-making process. Models may be verbal, pictorial, schematic, physical, scale, numerical and statistical or mathematical. In general, they attempt to describe the essence of a situation or activity by abstracting from reality so the decision maker can study the relationship among relevant variables in isolation. They do not attempt to duplicate reality in all respects, for models that do this reveal nothing. Instead, they are limited approximation of reality. If, for example, the system boundaries were defined in a wide and inclusive manner, the problem situation would perhaps be more realistic, but the problem itself would remain just as difficult to solve. The key to model building lies in abstracting only the relevant variables that affect the criteria and expressing the relationships in a testable form.

A generalized mathematical or statistical model might take the form:

Objective criteria = function of (controllable variables, uncontrollable variables, error)

or symbolically

Obj = f(X,Y,Є)

A full description of any model should also include a statement of its assumptions and constraints. All models need not have controllable X, uncontrollable Y, and error terms Є, but these are convenient classifications. The error term often represents a statistical factor which accounts for our use of sample rather than census data. Of course we attempt to keep the amount of error as small as possible.

As an example of a more specific mathematical model we might express a proposed production quantity Q as:

Q = f(F,D,I)

Where,

f = forecast or budgeted production rate

D = actual demand rate

I = current inventory level

Note that the forecast production rate F is a controllable variable, actual demand D is largely uncontrollable, and current inventory level I has elements of both. By relating the parameters F,D, and I, via appropriate equations and assigning values to these parameters, the model builder can arrive at proposed values for Q.

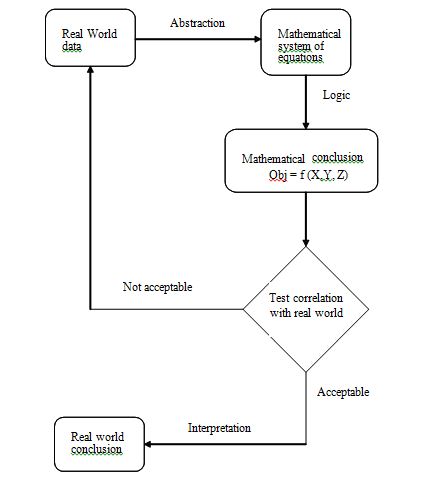

Fig. 4 shows the mathematical modeling process in the form of a schematic model [1:72 (modified)]. Note that it is an abstraction which begins and ends with the real world. The validity of a model should, of course, be judged relative to what it is supposed to do. If, for example, a forecasting model accurately predicts real world demand, a manager would consider it to be a “good” model. Techniques are available to evaluate the validity of models, some of which we shall discuss later in the text.

Fig.5. Mathematical models

One of the most difficult aspects of model building lies in incorporating experience, human values, and subjective or less-tangible factors into the relationship in a mathematical or statistical manner. Although this is certainly not a new problem, the renewed emphasis on human and social values has generated increased efforts along these lines. Another difficult aspect of model building involves the problems of accommodating multiple goals, as explained earlier. Whereas goal identification is still largely a subjective undertaking, the quantitative approaches of utility theory and goal programming offer some objective potential in this realm.

Any decision problem implies that alternatives exist. The relationships formulated between the parameters and the decision criteria permit the generation of alternative solutions (step-4) by varying the values of the parameters. Mathematical and statistical models, again, are particularly suitable for generating alternatives because they are so easily modified. The model builder can “experiment” with the model by substituting different values for controllable variables (such as employment levels) as well as uncontrollable variables (such as actual demand).

It is noted earlier that the goals and decision criteria had a strong value base. The generation of alternatives also has important value connotations. Just as goals are an end, the alternatives are a means to that end. Both individuals and institutions are sometimes faced with the question of whether or not a given means is morally acceptable.

Our society generally upholds the conviction that the end does not justify the means. For example, the courts have said that a legitimate goal of profits or market share does not justify price fixing or collusion as a means of obtaining it. In some cases, legislation (such as antitrust laws) may constitute a satisfactory behaviorual guide for managers. But laws do not anticipate every situation and managers must generally rely upon their individual and institutional value systems. In these situations values play an important role in the decision process by ruling out (as infeasible) any alternatives that are not consistent with behavioral standards.

The final step in the decision process ( step 5) is to choose the best course of action, that is, the one that best satisfies the criteria. Some models, such as linear programming, are inherently of an optimizing nature and automatically seek out a maximizing or minimizing solution. If the system boundaries are clearly defined, and all the model assumptions are satisfied, these methods will generate optimal solutions to the specific situations. Other models are more suitable for use in situations that are so complex, uncertain, or subjective that optimal solutions cannot be used to suggest the best course of action, or at least a preferred course, on the basis of the information and resources available to make the decision. The best course of action or solution to a problem determined through use of a model is just that-a solution to the model! The true test of the decision process comes when the theoretical solution is applied to the real-world situation. Decision-making processes should therefore incorporate follow-up procedures to ensure that the action is appropriate in the real world. These procedures should include an analysis and evaluation of the solution plus any recommendations for changes or adjustments.

2.3. Environment of Decisions: Certainty-Uncertainty

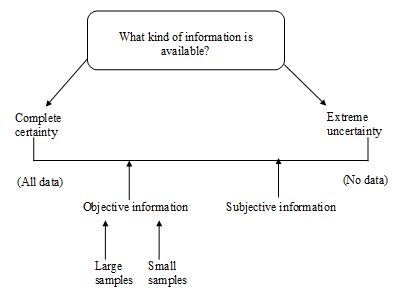

Focus on the knowledge and information base that provides the data which are essential to the scientific decision-making process is important. With better information, a decision maker can be expected to make decisions that more effectively move an organization towards its goals. Fig. 5 depicts the information environment of decisions as one ranging from a situation where the decision maker has (or assumes he or she has) complete information about the decision variables to the other extreme where he or she has no information about them. Operations management decisions are in fact made at numerous points along this continuum from complete certainty to extreme uncertainty.

As can be seen, complete certainty requires census data on all elements in the population. Lacking this, large samples lend more certainty than do small samples. Beyond this, subjective information is very likely better than no data at all.

Fig. 6. Information environment

Last modified: Thursday, 3 October 2013, 5:51 AM