Site pages

Current course

Participants

General

MODULE 1. Systems concept

MODULE 2. Requirements for linear programming prob...

MODULE 3. Mathematical formulation of Linear progr...

MODULE 5. Simplex method, degeneracy and duality i...

MODULE 6. Artificial Variable techniques- Big M Me...

MODULE 7.

MODULE 8.

MODULE 9. Cost analysis

MODULE 10. Transporatation problems

MODULE 11. Assignment problems

MODULE 12. waiting line problems

MODULE 13. Network Scheduling by PERT / CPM

MODULE 14. Resource Analysis in Network Scheduling

LESSON 3. Linear Programming – Basic Ideas

3.1 General Linear Programming Problem

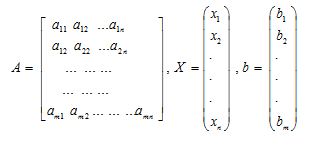

The linear programming involving more than two variables may be expressed as follows :

Maximize (or) Minimize Z = c1x1 + c2x2 + c3x3 + ....... cnxn

subject to the constraints

a11x1 + a12x2 + ... + a1n xn £ or = or ³ b1

a21x1 + a22x2 + ... + a2n xn £ or = or ³ b2

a31x1 + a32x2 + ... + a3n xn £ or = or ³ b3

................................

am1x1 + am2 x2 + ... + amn xn £ or = or ³ bm

and the non-negativity restrictions

x1, x2, x3, ... xn ³ 0.

Note : Some of the constraints may be equalities, some others may be inequalities of (£) type or (³) type or all of them are of same type.

Solution: A set of values x1, x2 ...xn which satisfies the constraints of the LPP is called its solution.

Feasible solution: Any solution to a LPP which satisfies the non-negativity restrictions of the LPP is called its feasible solution.

Optimum Solution or Optimal Solution: Any feasible solution which optimizes (maximizes or minimizes) the objective function of the LPP is called its optimum solution or optimal solution.

Slack Variables: If the constraints of a general LPP be

............(1)

............(1)

then the non-negative variables si which are introduced to convert the inequalities (1) to the equalities are called slack variables. The value of these variables can be interpreted as the amount of unused resource.

Surplus Variables: If the constraints of a general LPP be

............(2)

............(2)

then the non-negative variables si which are introduced to convert the inequalities (1) to the equalities

are called surplus variables. The value of these variables can be interpreted as the amount over and above the required level.

3.2 Canonical and Standard forms of LPP :

After the formulation of LPP, the next step is to obtain its solution. But before any method is used to find its solution, the problem must be presented in a suitable from. Two forms are dealt with here, the canonical form and the standard form.

The canonical form : The general linear programming problem can always be expressed in the following form :

Maximize Z = c1 x1 + c2 x2 + c3 x3 + ... cn xn

subject to the constraints

a11x1 + a12x2 + .... + a1n xn ≤ b1

a21x1 + a22x2 + .... + a2n xn ≤ b2

.................................

amlx1 + am2 x2 + ... + amn xn ≤ bm

and the non-negativity restrictions

x1, x2, x3, ... xn ≥ 0.

This form of LPP is called the canonical form of the LPP.

In matrix notation the canonical form of LPP can be expressed as :

Maximize Z = CX (objective function)

Subject to AX ≤ b (constraints)

and X ≥ 0 (non-negativity restrictions)

where C = (c1 c2 …cn),

3.2.2 Characteristics of the Canonical form :

(i) The objective function is of maximization type.

Min f(x) = - Max {-f(x) } (or)

Min Z = - Max (-Z)

(ii) All constraints are of (≤) type, except for the non-negative restrictions.

An inequality of “≥” type can be changed to an inequality of the type “≤” type by multiplying both sides of the inequality y -1.

For example, the linear constraint

a1lx1 + a12 x2 + ... + a1n xn ≥ bi

is equivalent to

-ailx1 - ai2 x2 - ... - ain xn ≤ - bi

An equation may be replaced by two weak inequalities in opposite directions.

For example

ailx1 + ai2 x2 + ... + ain xn = bi

is equivalent to

ailx1 + ai2 x2 + ... + ain xn ≥ bi

and ailx1 + ai2 x2 + ... + ain xn ≤ bi

(iii) All variables are non-negative.

A variable which is unrestricted in sign is equivalent to the difference between two non-negative variables. Thus if xj is unrestricted in sign, it can be replaced by (xjl- xjll), where xjland xjll are both non-negative,

i.e., xj = xjl- xjll, where xjl ≥ 0 and xjl l≥ 0

The Standard From :

The general linear programming problem in the form

Maximize or Minimize

Z = c1 x1 + c2 x2 + …….. + cn xn

Subject to the constraints

a11x1 + a12x2 + ....................... + a1n xn = b1

a21x1 + a22x2 + ....................... + a2n xn = b2

.....................................................................

amlx1 + am2 x2 + ............... + amn xn = bm

and x1, x2, ....................... xn ≥ 0 is known as standard form

In matrix notation the standard form of LPP can be expressed as :

Maximize or Minimize Z = CX (objective function)

Subject to constraints AX = b and X ≥ 0

Where, c = (c1,c2,…,cn),

3.2.3 Characteristics of the standard form :

All the constraints are expressed in the form of equations, except for the non-negative restrictions.

The right hand side of each constraint equation is non-negative.

The inequalities can be changed into equation by introducing a non-negative variable on the left hand side of such constraint. It is to be added (slack variable) if the constraint is of “ ≤ ” type and subtracted (surplus variable) if the constraint is of “ ≥ ” type.

Basic Solution.: Given a system of m simultaneous linear equations with n variables (m < n).

Ax=b, xT ε Rn

where A is an m x n matrix of rank m. Let B be any m x m sub matrix, formed by m linearly independent columns of A. Then a solution obtained by setting n-m variables not associated with the columns of B, equal to zero, and solving the resulting system, is called a basic solution to the given system of equations.

The m variables, which may be all different from zero, are called basic variables. The m x m non-singular sub matrix B called a basis matrix with the columns of B as basis vectors. The (n-m) variables which are put to zero are called as non-basic variables.

Example:

Obtain all the basic solutions to the following system of linear equation:

x1 + 2x2 + x3 = 4

2x1 + x2 + 5x3 = 5

Solution:

The given system of equations can be written in the matrix form

Ax=b

where,

since rank of A is 2, the maximum number of linearly independent columns of A is 2. Thus we can take any of the following, 2x 2 sub-matrices as basis matrix B:

The variables not associated with the columns of B are x3, x2 and x1 respectively, in the three different cases.

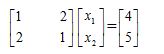

A basic solution to the given system is now obtained by setting x3 = 0, and solving the system

Thus a basic (non-basic) solution to the given system is

(Basic) x1= 2, x2 = 1; (Non-basic) x3 = 0,

(Basic) x1= 5, x3 = -1; (Non-basic) x2 = 0,

(Basic) x2 = 5/3, x3 = 2/3; (Non-basic) x1 = 0.

We observe that all the above three basic solutions are non-degenerate solution.

Degenerate Basic Solution: A basic solution is said to be a degenerate basic solution if one or more of the basic variables are zero.

Basic Feasible Solution: A feasible solution to a LPP., which is also a basic solution to the problem is called a basic feasible solution to the LPP.

Last modified: Monday, 28 April 2014, 11:44 AM